On February 20, 2026, the Supreme Court ruled in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act (IEEPA) does not grant the President authority to impose tariffs. Within hours, the White House issued an executive order terminating IEEPA-based duties. By February 22, U.S. Customs and Border Protection (CBP) halted collection of all IEEPA tariffs for entries on or after February 24, 2026.

That left a specific question for every American importer: what about the duties we already paid?

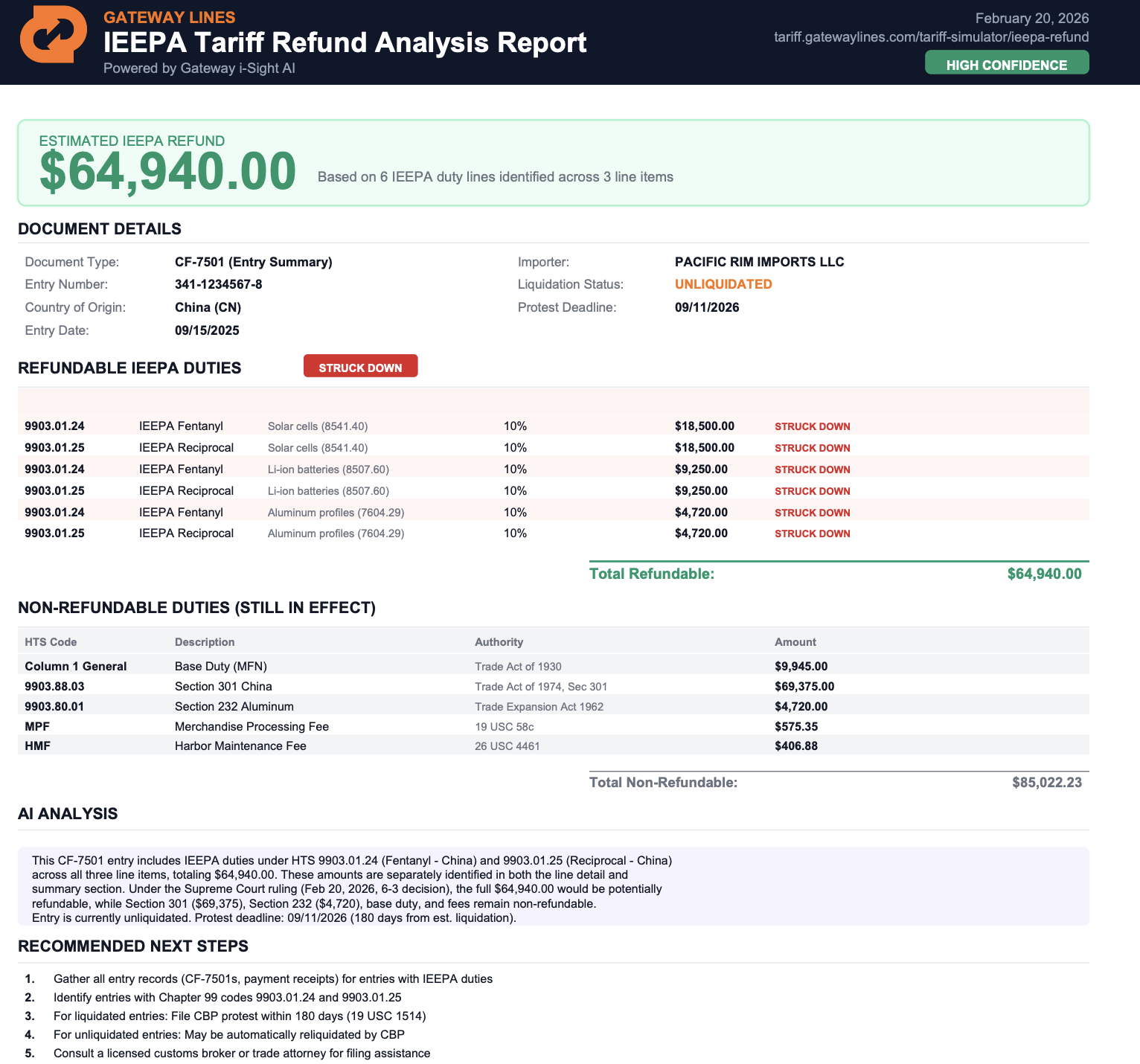

The answer arrived on April 20, 2026, when CBP launched the Customs Adjustment and Post-Entry (CAPE) portal — a digital filing system that opened the formal refund pathway for IEEPA duties paid before the SCOTUS ruling.

For importers with significant China sourcing or any volume from Brazil, Russia, Iran, Venezuela, or Cuba during the affected period, the dollars on the table are not small. This guide walks through exactly which IEEPA tariff actions ended, how the CAPE portal works, who qualifies for refunds, and what to do next.

What Got Struck Down: The IEEPA Tariff Actions That Ended

The Trump administration used IEEPA to impose several distinct tariff regimes. The Supreme Court's Learning Resources ruling and the subsequent executive order ended all of them. The largest categories included:

The IEEPA "trafficking" tariffs on Mexico, Canada, and China — Originally imposed in early 2025 citing fentanyl and migration concerns. These duties added 10–25% on top of normal tariff rates for affected goods.

Country-specific IEEPA actions on Brazil — A 40% additional ad valorem duty imposed under IEEPA authority on certain Brazilian imports.

Secondary sanctions tariffs — Threatened or imposed against countries trading with Cuba, Venezuela, Russia, and Iran.

Reciprocal tariff frameworks built on IEEPA — Several country-specific reciprocal tariff arrangements relied on IEEPA as the underlying legal authority.

CBP guidance issued February 22 confirmed that collection ceased for entries on or after 12:00 a.m. EST February 24, 2026. The same guidance opened the door for refunds on duties already paid.

Important: Section 232, Section 301, the Section 122 surcharge (added February 24, 2026), and the de minimis suspension are NOT affected by this ruling. Those tariffs remain in full force and have nothing to do with IEEPA.

What the CAPE Portal Actually Is

CAPE — Customs Adjustment and Post-Entry — is CBP's digital filing system specifically built for IEEPA refund claims following the Learning Resources ruling.

Before CAPE, the only path for tariff refunds was the traditional protest process under 19 U.S.C. § 1514, which requires line-by-line entry-summary protests filed within 180 days of liquidation. That process is slow, paperwork-heavy, and designed for one-off corrections rather than mass refunds across an entire tariff regime.

The CAPE portal is different. It's purpose-built for the scale of the IEEPA reversal. Importers (or their licensed customs brokers) can:

Submit refund requests in bulk across multiple entries

Upload supporting entry summaries (CBP Form 7501) and commercial invoices

Track filing status digitally

Receive refund disbursements through their existing ACH or check arrangements with Treasury

The portal is accessible at aceaccountreview.cbp.gov through the standard ACE (Automated Commercial Environment) login. Importers without ACE accounts must establish one — which has its own backlog (something Gateway has direct experience navigating).

Who Qualifies: The Eligibility Criteria

Refund eligibility depends on three factors: what you imported, when you imported it, and how the duties were classified.

Who can file

Any importer of record who paid IEEPA duties on entries between the original effective date of each IEEPA action and February 24, 2026, can file. This includes:

U.S. companies importing for resale or internal use

Foreign sellers acting as importer of record under DDP arrangements

Customs brokers filing on behalf of clients

What entries qualify

The duty must have been collected under one of the terminated IEEPA actions. The key indicator on your CBP Form 7501 (Entry Summary) is the Chapter 99 HTS code applied. Specifically:

HTS 9903.01.xx range — IEEPA China and trafficking actions

HTS 9903.02.xx range — IEEPA Brazil actions

Various 9903.xx codes tied to country-specific IEEPA orders

If your Form 7501 shows Section 301 codes (9903.88.xx) or Section 232 codes (9903.79–9903.95 ranges), those are separate tariff regimes and not affected.

The date window

The earliest IEEPA tariff actions were imposed in early 2025. The latest applicable entry date is February 23, 2026 (the day before CBP halted collection). Goods loaded onto a vessel before February 24 but entered for consumption between February 24 and February 28 fall under a transitional in-transit exception that Treasury has indicated is also refundable.

The Section 122 wrinkle

This is where many importers get confused. After IEEPA was struck down on February 20, the White House replaced part of the lost tariff revenue with a Section 122 temporary import surcharge of 10%, effective February 24, 2026. Section 122 is a different statutory authority and is not subject to the Supreme Court ruling.

Practically, this means:

IEEPA duties paid before February 24, 2026 → refundable through CAPE

Section 122 surcharge paid on or after February 24, 2026 → not refundable, currently in effect through July 24, 2026

If your customs broker already updated your filings to reflect the new regime, you'll see this transition clearly in your entry summaries.

How to Estimate What You're Owed

The math for IEEPA refunds is straightforward in concept and tedious in execution. For each qualifying entry:

Refund per entry = (declared customs value) × (IEEPA duty rate applied)

So a $250,000 entry from China with a 25% IEEPA additional duty means a $62,500 refund on that single entry. Multiply across hundreds of entries over a multi-year window, and the totals get serious quickly.

The challenge is that most companies don't have a clean, line-by-line record of which Chapter 99 codes applied to which entries — especially if they used multiple customs brokers over the period or had broker turnover.

This is why we built the Gateway IEEPA Refund Calculator. It scans entry-summary data and identifies which entries carry refund-eligible IEEPA codes, then calculates the total estimated refund across your entire import history. No signup. No commitment. The tool returns a refund estimate within minutes.

The calculator covers all 30,000+ HTS codes and properly distinguishes IEEPA duties (refundable) from Section 301, 232, and 122 (not refundable). For importers with legitimate refund eligibility, it surfaces the number before you decide whether to commit time to the full filing process.

How to File: The CAPE Portal Process

Once you've estimated your refund, the filing process through CAPE follows these steps:

Step 1: Establish ACE Portal Access

If your company doesn't already have an ACE account, you'll need to create one. The application process can take days to weeks depending on backlog. Existing importers with ACE accounts can skip this step.

Step 2: Compile Your Entry Records

You'll need:

CBP Form 7501 (Entry Summary) for each affected entry

Commercial invoices and packing lists

Bill of lading and arrival notices

Any prior protests or post-entry amendments already filed

Most licensed customs brokers can pull this data directly from ACE for you. If you're working with multiple brokers, consolidate the records before filing.

Step 3: Submit Through CAPE

The CAPE portal accepts both single-entry and batch submissions. For most importers with more than 20 entries to claim, the batch upload is dramatically faster. Each claim must include:

Entry number and port of entry

Date of entry and liquidation status

Original duty paid and refund amount requested

Supporting documentation in PDF format

Step 4: Track and Receive Disbursement

CBP has indicated processing times of 60–120 days for routine refund claims. Refunds are issued through the same payment method you originally used for duty payment (ACH for most commercial importers, check for some legacy arrangements).

Step 5: Monitor for Audit

CBP retains the right to audit refund claims for accuracy. Keep all supporting records for at least five years post-refund. Honest claims with complete documentation rarely trigger issues; cherry-picked or inflated claims do.

Common Mistakes Importers Make

A few patterns are already emerging from early CAPE filings:

Confusing Section 301 with IEEPA. Both target China-origin goods. Both add additional duties on top of normal tariffs. But only IEEPA was struck down. If your entries show Chapter 99 HTS codes in the 9903.88.xx range, those are Section 301 and remain in effect.

Missing the in-transit window. Goods loaded before February 24 but entered between February 24 and February 28 may qualify under the transitional exception. Many importers are missing these claims.

Filing without consolidating broker records. Companies that used multiple customs brokers over the IEEPA period are often filing partial claims because they don't have a unified view of all entries. Pulling consolidated ACE data first prevents leaving money behind.

Waiting too long. While CAPE doesn't currently impose a hard deadline beyond the standard statute of limitations on refund claims, processing priority and CBP attention will favor early filers. Late filers may face longer review windows.

Assuming the refund is automatic. It isn't. CBP is not proactively refunding overpaid IEEPA duties. You have to file a claim through CAPE to receive the refund.

What This Means for Your 2026 Import Strategy

Beyond the immediate refund opportunity, the Learning Resources ruling and the subsequent Section 122 substitution have reshaped the U.S. tariff landscape in ways every importer should understand:

Section 122's 10% surcharge sunsets July 24, 2026. Unless extended by Congress, the surcharge expires. Imports landing after that date may face a meaningfully different cost structure.

Section 232 has expanded sharply. New Section 232 actions on patented pharmaceuticals (April 2026), advanced semiconductors (January 2026), processed critical minerals, and timber/lumber/furniture/cabinets (October 2025) are now in effect or scheduled. Section 232 is not subject to the IEEPA ruling.

Section 301 China tariffs remain unchanged. The original 2018 Section 301 framework, including Lists 1–4A and the 2024 EV/battery/solar additions, was unaffected by Learning Resources.

Trade strategy is now tariff strategy. With this much policy volatility, importers who model landed cost dynamically — across multiple regimes simultaneously — have a meaningful cost advantage over those still relying on annual rate sheets from their forwarders.

This is precisely why Gateway built tariff intelligence directly into its platform. Every shipment in your Gateway terminal is automatically scanned against the current tariff stack — IEEPA refund eligibility on past entries, Section 122 application on current entries, Section 232 sectoral tariffs by HTS code, and Section 301 China-origin treatment — without you having to track any of it manually.

What to Do This Week

If your company imports any meaningful volume:

Estimate your refund. Run your import history through the Gateway IEEPA Refund Calculator. It takes a few minutes and gives you a defensible number before you commit time to filing.

Confirm CAPE access. If your company doesn't have ACE portal access, start the application now. Backlogs run weeks.

Pull your historical entry data. Whether you file refunds yourself or through a customs broker, having a clean consolidated view of every entry in the IEEPA window is the foundation of a successful claim.

Distinguish IEEPA from everything else. Make sure your team understands which Chapter 99 codes are refundable (IEEPA) and which aren't (Section 301, 232, 122).

File before the queue gets longer. CAPE is processing claims now. Earlier filers will see disbursements faster.

The IEEPA refund window is the most significant trade-policy reset for U.S. importers in years. Companies that move on it early will recover real working capital. Those who wait — or who never realize they're owed money — won't.